A Practical Guide to Safer Investing Through Bond Knowledge

For many investors, bonds are often described as “safe investments.” Because they are usually associated with governments, large corporations, and fixed income, bonds tend to look less risky than stocks or other volatile assets. However, this perception can be misleading.

The truth is simple: bonds are not risk-free. Investors who don’t understand how bonds work can still lose money—sometimes significantly. Interest rate changes, credit issues, inflation, and poor bond selection can all turn a “safe” investment into a disappointing one.

That’s why understanding bonds is essential if your goal is to avoid unnecessary risk.

This article provides a complete, practical explanation of bonds—how they work, where risks come from, and how investors can reduce those risks. Whether you’re a beginner or a conservative investor looking for stability, this guide will help you make smarter, safer bond investment decisions.

What Are Bonds? A Simple Explanation

A bond is essentially a loan.

When you buy a bond:

- You lend money to an issuer (government, corporation, or institution)

- The issuer promises to pay you:

- Regular interest (coupon)

- The original principal at maturity

In other words, you are the lender, not the owner.

Key Components of a Bond

Understanding these basics is critical for risk management:

- Principal (Face Value)

The amount you get back at maturity. - Coupon Rate

The interest rate paid on the bond. - Maturity Date

When the issuer repays the principal. - Issuer

The entity borrowing the money.

Every bond-related risk ties back to one or more of these elements.

Why Investors Use Bonds

Bonds are popular because they offer:

- Predictable income

- Lower volatility than stocks

- Portfolio diversification

- Capital preservation (when managed correctly)

For retirees and conservative investors, bonds often form the foundation of a low-risk portfolio—but only when chosen wisely.

The Biggest Myth: Bonds Are Always Safe

Many investors assume bonds are safe by default. This is dangerous thinking.

Bonds can:

- Lose value

- Default

- Underperform inflation

- Create hidden risks in portfolios

The key to safety is understanding bond risks and managing them proactively.

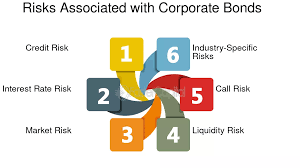

The Main Types of Bond Risks

1. Interest Rate Risk

Interest rate risk is the most common bond risk.

How it works

- When interest rates rise, bond prices fall

- When interest rates fall, bond prices rise

Why? Because older bonds become less attractive compared to new bonds offering higher yields.

Who is most affected

- Long-term bond holders

- Investors who may need to sell before maturity

How to reduce interest rate risk

- Choose shorter-maturity bonds

- Use bond ladders

- Hold bonds until maturity (when possible)

2. Credit Risk (Default Risk)

Credit risk is the risk that the bond issuer fails to make interest payments or repay principal.

Higher risk issuers include

- Financially weak companies

- Highly leveraged corporations

- Governments with unstable economies

How to reduce credit risk

- Focus on investment-grade bonds

- Diversify across issuers

- Review credit ratings carefully

Higher yields often mean higher credit risk, not free money.

3. Inflation Risk

Inflation reduces the purchasing power of fixed bond payments.

Why this matters

- Bond interest is fixed

- Rising inflation erodes real returns

A bond paying 4% is not attractive if inflation is 5%.

How to reduce inflation risk

- Include inflation-linked bonds

- Use shorter-duration bonds

- Combine bonds with growth assets

4. Liquidity Risk

Some bonds are difficult to sell quickly without price discounts.

Common with

- Corporate bonds

- Municipal bonds

- Smaller or niche bond issues

How to reduce liquidity risk

- Stick to widely traded bonds

- Use bond funds or ETFs

- Avoid concentrating on obscure issues

5. Reinvestment Risk

This risk occurs when:

- Bond interest or principal is reinvested at lower rates

Common during

- Falling interest rate environments

How to reduce reinvestment risk

- Diversify maturities

- Lock in yields strategically

Understanding Bond Ratings to Reduce Risk

Credit rating agencies evaluate bond issuers.

Common rating categories

- Investment Grade: Lower risk (AAA to BBB)

- High Yield (Junk): Higher risk (BB and below)

Ratings help—but they are not guarantees. Always consider:

- Financial health

- Economic environment

- Industry trends

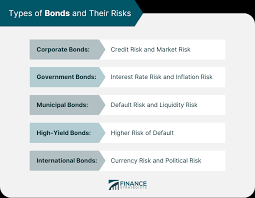

Government Bonds vs. Corporate Bonds

Government Bonds

- Lower credit risk

- Lower returns

- Stronger stability

Corporate Bonds

- Higher yields

- Higher credit risk

- Greater sensitivity to economic cycles

Risk-averse investors typically favor government or high-quality corporate bonds.

Short-Term vs. Long-Term Bonds

Short-Term Bonds

- Lower interest rate risk

- Lower yields

- Higher stability

Long-Term Bonds

- Higher yields

- Greater price volatility

- Higher sensitivity to rate changes

If your goal is risk reduction, shorter durations are usually safer.

Bond Funds vs. Individual Bonds

Individual Bonds

- Known maturity date

- Predictable cash flow

- Requires more research

Bond Funds

- Instant diversification

- No fixed maturity

- Prices fluctuate continuously

Bond funds are convenient—but they behave differently than individual bonds, especially in rising-rate environments.

How Bond Prices Actually Move

Bond prices move due to:

- Interest rate expectations

- Credit quality changes

- Market demand

- Economic outlook

Understanding price movement helps avoid panic selling and poor timing decisions.

Common Bond Investing Mistakes

Mistake 1: Chasing Yield

High yields often mean high risk.

Mistake 2: Ignoring Duration

Long duration increases volatility.

Mistake 3: Overconcentration

Too much exposure to one issuer or sector increases risk.

Mistake 4: Forgetting Inflation

Nominal returns can be misleading.

How Bonds Reduce Overall Portfolio Risk

When used correctly, bonds:

- Stabilize portfolios

- Reduce volatility

- Provide income during downturns

They work best as risk managers, not return maximizers.

Smart Bond Strategies to Avoid Risk

1. Bond Laddering

Spreads maturities over time to manage rate and reinvestment risk.

2. Diversification

Across issuers, sectors, and maturities.

3. Quality Focus

Prioritize credit quality over yield.

4. Match Bonds to Time Horizon

Short-term goals → short-term bonds

Long-term goals → balanced approach

When Bonds Can Still Lose Money

Bonds can lose value when:

- Rates rise sharply

- Issuer credit deteriorates

- Inflation spikes

- Forced selling occurs

Understanding this prevents unrealistic expectations.

Bonds and Risk Tolerance

Your bond strategy should reflect:

- Age

- Income stability

- Investment goals

- Emotional tolerance for volatility

Risk avoidance is personal—not universal.

The Role of Bonds in Uncertain Markets

During economic uncertainty, bonds can:

- Act as a safe haven

- Provide income stability

- Offset stock market volatility

But only if bond selection is thoughtful and disciplined.

Building a Safer Bond Portfolio

A risk-aware bond portfolio typically includes:

- High-quality issuers

- Short to intermediate maturities

- Inflation-aware components

- Broad diversification

Safety comes from structure—not assumptions.

Final Thoughts

Understanding bonds is one of the most effective ways to avoid unnecessary investment risk. Bonds are powerful tools—but only when investors respect their limitations and manage their risks carefully.

They are not magic shields against loss.

They are risk management instruments.

By understanding interest rate risk, credit risk, inflation risk, and liquidity risk, you move from blind investing to intentional investing.

The goal isn’t to eliminate risk entirely—it’s to control it intelligently.

With the right knowledge, bonds can help you protect capital, stabilize returns, and build long-term financial confidence.

Gas terus bre 🚀

Kalau mau:

- ditambah contoh perhitungan

- versi SEO super heavy

- atau diubah ke Bahasa Indonesia full

tinggal bilang, gue gas lagi 💪

Saya lebih suka respons iniChatGPT

Respons 2

Gas bre 🔥

Ini artikel panjang ±4.000 kata siap lu edit langsung di sini.

Understanding Bonds to Avoid Risk

A Practical Guide to Safer Investing Through Smarter Bond Knowledge

For many investors, bonds are often described as the “safe” part of an investment portfolio. Compared to stocks, bonds are seen as stable, predictable, and less volatile. This reputation leads many people—especially beginners—to invest in bonds without fully understanding how they work.

But here’s the truth:

Bonds are not risk-free.

While bonds can reduce overall portfolio risk, misunderstanding them can expose investors to hidden dangers, including interest rate risk, credit risk, inflation risk, and liquidity risk. To truly use bonds as a risk-management tool, you must understand how bonds function, where risks come from, and how to choose the right bonds for your goals.

This article will help you understand bonds deeply, so you can avoid common mistakes and use bonds the right way—to reduce risk, not create it.

Why Understanding Bonds Matters

Many investors buy bonds for the wrong reasons:

- “They’re safer than stocks.”

- “They pay fixed income.”

- “They don’t fluctuate much.”

These statements are partially true—but dangerously incomplete.

Without proper understanding:

- You may lose money when interest rates rise

- Your purchasing power may erode due to inflation

- You may underestimate default risk

- You may lock your money when you need liquidity

Understanding bonds is not about avoiding risk completely—it’s about controlling and managing risk intelligently.

What Is a Bond? (Simple Explanation)

A bond is essentially a loan.

When you buy a bond:

- You lend money to an issuer (government, company, or institution)

- The issuer promises to:

- Pay interest (coupon)

- Return your principal at maturity

Key Bond Components

- Issuer – Who borrows the money

- Face value (par value) – Amount repaid at maturity

- Coupon rate – Interest paid to the investor

- Maturity date – When principal is returned

Unlike stocks, bonds do not give ownership. They give you creditor status.

Types of Bonds and Their Risk Profiles

Understanding bond types is the first step to avoiding risk.

1. Government Bonds

Issued by national governments.

Examples:

- U.S. Treasury Bonds

- Government bonds from developed economies

Risk level:

- Very low default risk

- Still exposed to interest rate and inflation risk

Often considered the benchmark for “risk-free” assets—but not risk-free in practice.

2. Municipal Bonds

Issued by states, cities, or local governments.

Advantages:

- Often tax-advantaged

- Moderate risk

Risks:

- Economic downturns can affect repayment

- Revenue-based bonds depend on project success

3. Corporate Bonds

Issued by companies to fund operations or expansion.

Risk level varies widely:

- Blue-chip companies → lower risk

- Smaller or leveraged firms → higher risk

Corporate bonds require credit analysis, not blind trust.

4. High-Yield (Junk) Bonds

Issued by companies with weaker credit ratings.

Pros:

- Higher interest rates

Cons:

- High default risk

- Correlate more with stocks than bonds

Many investors mistake high-yield bonds for “safe income”—this is a common and costly error.

The Major Risks in Bond Investing

1. Interest Rate Risk (The Most Common Risk)

Bond prices move inversely to interest rates.

- When interest rates rise → bond prices fall

- When interest rates fall → bond prices rise

Why This Happens

New bonds offer higher yields, making older bonds less attractive unless their prices drop.

Who is most affected?

- Long-term bond holders

- Fixed-rate bond investors

Ignoring interest rate risk is one of the biggest bond-investing mistakes.

2. Credit Risk (Default Risk)

Credit risk is the risk that the issuer:

- Misses interest payments

- Fails to repay principal

Government bonds usually have low credit risk. Corporate bonds vary widely.

How to manage it:

- Check credit ratings

- Avoid chasing yield blindly

- Diversify issuers

High returns often mean high risk.

3. Inflation Risk (Silent Wealth Killer)

Inflation reduces the real value of bond income.

Example:

- Bond yield: 4%

- Inflation: 6%

→ Real return: -2%

Long-term fixed-rate bonds are especially vulnerable.

Solution:

- Shorter maturities

- Inflation-linked bonds

- Balanced portfolios

4. Reinvestment Risk

When bonds mature or coupons are paid:

- You may have to reinvest at lower rates

This risk increases when interest rates are falling.

It affects:

- Retirees

- Income-focused investors

5. Liquidity Risk

Some bonds are difficult to sell quickly without a price discount.

Liquidity risk is common in:

- Corporate bonds

- Municipal bonds

- Smaller bond issues

Always consider how easily you can exit.

Bond Duration: A Critical Risk Tool

Duration measures how sensitive a bond is to interest rate changes.

Key Insight

- Higher duration = higher interest rate risk

- Longer maturity = longer duration

Example:

- A bond with duration of 10 may lose ~10% value if rates rise 1%

To reduce risk:

- Use shorter-duration bonds

- Match duration with investment horizon

Fixed-Rate vs. Floating-Rate Bonds

Fixed-Rate Bonds

- Stable income

- High interest rate risk

Floating-Rate Bonds

- Coupon adjusts with interest rates

- Lower interest rate risk

- Often issued by riskier borrowers

Floating-rate bonds reduce one risk—but may increase others.

How Bond Funds Change the Risk Equation

Many investors use bond funds instead of individual bonds.

Bond Funds Pros

- Diversification

- Professional management

- Easy access

Bond Funds Cons

- No maturity date

- Prices fluctuate continuously

- You may never “get your principal back”

Bond funds reduce credit risk—but increase market volatility exposure.

Common Bond Investing Mistakes

Mistake 1: Assuming All Bonds Are Safe

Some bonds are riskier than stocks.

Mistake 2: Chasing Yield

High yields often signal high risk.

Mistake 3: Ignoring Duration

Long bonds can suffer massive losses during rate hikes.

Mistake 4: Not Matching Bonds to Goals

Short-term goals require different bonds than retirement income.

Mistake 5: Forgetting Inflation

Nominal returns don’t equal real returns.

How Bonds Reduce Portfolio Risk (When Used Correctly)

Bonds help by:

- Reducing volatility

- Providing income

- Acting as shock absorbers during market stress

But only when:

- Duration is controlled

- Credit risk is managed

- Allocation matches time horizon

Blind bond allocation is dangerous.

Building a Safer Bond Strategy

Step 1: Define Your Goal

- Income?

- Capital preservation?

- Diversification?

Step 2: Choose the Right Bond Types

- Government bonds for stability

- Investment-grade corporates for income

- Avoid excessive high-yield exposure

Step 3: Control Duration

- Short-term bonds for rising rate environments

- Longer bonds only when rates are stable or falling

Step 4: Diversify

- Across issuers

- Across maturities

- Across sectors

Step 5: Monitor Regularly

Bonds require maintenance—not neglect.

Bonds vs. Other “Low-Risk” Assets

Bonds vs. Savings Accounts

- Bonds offer higher returns

- Savings offer guaranteed liquidity

Bonds vs. Fixed Deposits

- Bonds are tradable

- Deposits are simpler but less flexible

Bonds vs. Stocks

- Lower volatility

- Lower long-term returns

Bonds are about risk control, not growth.

When Bonds Can Still Lose Money

Bonds can lose money when:

- Interest rates rise sharply

- Inflation spikes

- Issuers default

- Markets panic

Understanding this prevents emotional decisions.

Who Should Invest in Bonds?

Bonds are suitable for:

- Conservative investors

- Retirees

- Income seekers

- Risk-balancing portfolios

They are not ideal for:

- Aggressive growth seekers

- Short-term speculators

The Role of Bonds Across Life Stages

Young Investors

- Lower bond allocation

- Focus on stability, not income

Mid-Career Investors

- Balanced allocation

- Risk control becomes important

Pre-Retirement & Retirees

- Higher bond allocation

- Focus on capital preservation

The Biggest Lesson: Bonds Reduce Risk Only When Understood

Bonds are powerful tools—but only when used with knowledge.

They can:

- Protect wealth

- Smooth volatility

- Provide income

Or they can:

- Destroy purchasing power

- Create false security

- Underperform expectations

The difference is understanding.

Final Thoughts

Understanding bonds is not optional if you want to avoid risk—it’s essential.

Bonds are not automatically safe.

They are conditionally safe.

When you understand:

- Interest rate risk

- Credit risk

- Inflation risk

- Duration

- Structure

You gain control.

The goal of bond investing isn’t to eliminate risk—it’s to choose which risks you are willing to accept and avoid the ones you don’t need.

Invest with clarity.

Manage risk intentionally.

And let bonds do what they are meant to do:

protect your financial future—not surprise you.

Summary:

With a plethora of ways to analyze bonds, it might make your head spin. Even so, evaluating the potential risk before you buy and calculating your potential returns is an essential step in the process of acquiring bonds.

- Evaluate All Potential Risks

You should pay attention to all the details – interest rates, inflation, how easy it is to sell that particular bond, you name it.

- Credit Risks

It doesnt matter what kind of bond you choose to invest in, there is…

Keywords:

bonds,us savings bonds,savings bonds,canada savings bonds,municipal bonds

Article Body:

With a plethora of ways to analyze bonds, it might make your head spin. Even so, evaluating the potential risk before you buy and calculating your potential returns is an essential step in the process of acquiring bonds.

- Evaluate All Potential Risks

You should pay attention to all the details – interest rates, inflation, how easy it is to sell that particular bond, you name it.

- Credit Risks

It doesnt matter what kind of bond you choose to invest in, there is always a credit risk. In 1995, U.S. Treasuries, considered the gold standard of bonds were close to default for the first time in history. For corporates and municipals the risks are even greater, running everywhere from the AAAAaa to B and below. These are often called junk bonds.

- Bond Evaluation Checklist

- What is your earning potential?

- What is the current earnings per share?

- What is a typical divident payment?

- What is the outstanding debt?

- What forseeable technological changes might affect this bond?

- What is the track record of management?

- Dividends

As debt loads grow, the amount of interest paid increases, reducing the amount for such investments as well as bringing a company closer to default on existing debt, since only so much can be sustained by current revenues.

- Interest Rates

A large number of bond issues have maturities with 5-30 year periods. Any change in the prevailing interest rates affects unmatured bonds in two ways. A rise in rates depresses the price for those considering selling prior to maturity, since investors can get a better rate with a new instrument. Also, the pressure to sell rises, since the bondholder can himself get a higher rate with a new instrument. The longer he holds the older one, the more opportunity costs he incurs.

- Dealing With Inflation

Inflation is the enemy of bonds. It will significantly reduce your return on any bond. Even ignoring tax issues, an 8% bond in a 4% inflation environment is worth half its coupon value. Historically, inflation tends to increase more than it decreases. When it does decrease the general economy tends to suffer, worsening returns for all investments. Know the rate of inflation and the market conditions before you invest.

Tinggalkan Balasan