Bankruptcy is one of the most feared financial outcomes for individuals and households. It represents not only a legal process to resolve overwhelming debt but also a profound impact on your financial stability, creditworthiness, and long-term opportunities. However, bankruptcy is not inevitable. With foresight, discipline, and strategic action, it is possible to prevent financial collapse and regain control over your money.

This guide explores three simple yet highly effective ways to avoid bankruptcy, providing actionable advice and practical tools to maintain financial stability. These strategies focus on proactive planning, disciplined management, and informed decision-making.

Understanding Bankruptcy

1. What Bankruptcy Really Means

Bankruptcy is a legal declaration that an individual or business is unable to repay outstanding debts. It typically involves:

- Liquidation – Selling assets to pay creditors.

- Reorganization – Restructuring debt payments under court supervision.

- Legal Protections – Preventing creditors from taking immediate action.

While bankruptcy can provide a fresh start, it comes at significant costs:

- Severe Credit Impact – Bankruptcy remains on credit reports for 7–10 years.

- Financial Restrictions – Difficulty obtaining loans, mortgages, or credit cards.

- Psychological Stress – The stigma and emotional toll of financial failure.

Avoiding bankruptcy preserves financial freedom, opportunities, and peace of mind.

The Core Problem: Why People Approach Bankruptcy

Bankruptcy is rarely caused by a single factor. Common contributors include:

- Overspending – Living beyond income leads to debt accumulation.

- High-Interest Debt – Credit cards, payday loans, and predatory lending create compounding obligations.

- Unexpected Expenses – Medical emergencies, repairs, or job loss trigger debt spirals.

- Poor Financial Planning – Lack of budgeting, savings, or risk management.

- Economic Factors – Inflation, interest rate changes, and market downturns.

By addressing these issues proactively, individuals can prevent financial collapse and avoid bankruptcy.

3 Simple Ways to Avoid Bankruptcy

1. Create a Realistic and Detailed Budget

A budget is the foundation of financial stability and the first line of defense against bankruptcy.

Why Budgeting Matters

- Awareness – Understanding income and expenses prevents overspending.

- Control – Enables strategic allocation for debt repayment, savings, and essentials.

- Early Warning – Identifies financial shortfalls before they become critical.

Steps to Build an Effective Budget

- Track All Income – Include salaries, side income, investments, and irregular cash flows.

- List Fixed Expenses – Rent, mortgage, utilities, insurance, and debt payments.

- List Variable Expenses – Groceries, transportation, entertainment, and discretionary spending.

- Allocate Savings and Debt Repayment – Set aside funds for emergency savings and extra debt payments.

- Review and Adjust Monthly – Update the budget according to changing circumstances.

A realistic budget ensures that spending aligns with income, reducing the likelihood of debt accumulation and financial crises.

Practical Tips

- Use budgeting apps or spreadsheets for transparency.

- Implement the “50/30/20 Rule”: 50% for needs, 30% for wants, 20% for savings and debt repayment.

- Avoid impulse purchases by implementing a 24-hour waiting rule.

2. Manage Debt Strategically

Debt is often the gateway to bankruptcy. Managing it proactively is essential.

Understand Your Debt

- List all outstanding debts: credit cards, loans, mortgages, auto loans, student loans.

- Record interest rates, minimum payments, and total balances.

Debt Reduction Strategies

- Avalanche Method – Prioritize paying off the highest-interest debt first. This minimizes total interest over time.

- Snowball Method – Focus on the smallest debts first to build psychological momentum.

- Debt Consolidation – Combine multiple debts into one loan with lower interest to simplify repayment.

- Negotiate with Creditors – Request lower interest rates, extended payment plans, or temporary relief during hardship.

Avoid Debt Traps

- Limit new credit card usage.

- Avoid payday loans and predatory lending.

- Ensure any borrowing is essential and affordable.

Proper debt management prevents balances from spiraling out of control, a common pathway to bankruptcy.

3. Build an Emergency Fund

Unexpected expenses are a major cause of financial distress. An emergency fund acts as a financial safety net.

Why an Emergency Fund Works

- Covers unforeseen expenses without relying on credit.

- Reduces financial stress during emergencies.

- Provides flexibility and peace of mind.

How to Build an Emergency Fund

- Start Small – Begin with a goal of $500–$1,000 to cover minor emergencies.

- Target 3–6 Months of Expenses – Gradually build a fund sufficient to cover essential living costs.

- Separate the Fund – Keep it in a high-yield savings account, away from everyday spending.

- Automate Savings – Set up automatic transfers to ensure consistency.

Even modest emergency savings prevent new debt from accumulating and provide a buffer against financial shocks.

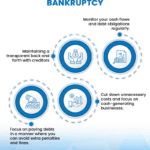

Supplementary Strategies to Strengthen Financial Stability

While the three methods above are the most crucial, additional strategies enhance financial resilience:

- Increase Income – Side jobs, freelance work, or investments supplement cash flow.

- Cut Unnecessary Expenses – Review subscriptions, memberships, and discretionary spending.

- Monitor Credit Reports – Stay informed of credit usage and errors to avoid surprises.

- Seek Professional Advice – Financial advisors or credit counselors can provide personalized solutions.

- Practice Mindful Spending – Align purchases with needs and long-term goals.

These strategies complement budgeting, debt management, and emergency savings to reinforce financial security.

The Psychological Benefits of Avoiding Bankruptcy

Preventing bankruptcy isn’t just about money; it also impacts mental well-being:

- Reduced Stress – Financial control reduces anxiety.

- Improved Relationships – Less money-related conflict in households.

- Confidence in Decision-Making – Ability to plan for the future without fear of collapse.

- Long-Term Peace of Mind – Secure finances foster emotional stability and life satisfaction.

A proactive approach transforms financial discipline into psychological resilience.

Case Study: Breaking the Bankruptcy Cycle

Consider John, who faced high credit card debt and a sudden medical expense:

- Budgeting – John tracked every expense and realized overspending on non-essentials.

- Debt Management – He implemented the avalanche method, paying off the highest-interest cards first.

- Emergency Fund – He saved small amounts weekly to create a buffer for future emergencies.

- Discipline – He avoided new debt and monitored his progress monthly.

Over two years, John eliminated high-interest debt, built an emergency fund, and avoided bankruptcy, demonstrating the effectiveness of these simple strategies.

Long-Term Financial Planning

Avoiding bankruptcy is not a one-time action but a lifestyle:

- Plan for Major Expenses – Save for home, education, or major purchases rather than relying on credit.

- Invest for Growth – Once debt is under control, focus on building wealth and financial independence.

- Review Finances Regularly – Adapt plans as income, expenses, or life circumstances change.

- Teach Financial Literacy – Educate family members to ensure long-term financial health.

Sustainable financial planning protects against future crises and ensures long-term stability.

Conclusion

Bankruptcy is a serious financial setback, but it is not inevitable. By taking proactive steps, individuals can maintain control of their finances, prevent overwhelming debt, and preserve both financial and emotional well-being.

Key Takeaways:

- Create a Detailed Budget – Track income and expenses, prioritize essential payments, and avoid overspending.

- Manage Debt Strategically – Use methods like avalanche, snowball, consolidation, and negotiation to reduce debt efficiently.

- Build an Emergency Fund – Save 3–6 months of expenses to handle unforeseen events without relying on credit.

Supplement these strategies with additional practices like mindful spending, income growth, credit monitoring, and professional advice. By doing so, you can stop the cycle of financial stress, preserve your creditworthiness, and secure a stable, prosperous future.

Summary:

In this debt-ridden society, many people are in severe financial difficulties. While bankruptcy is the last step in a long road of financial pressures for many, others opt for this solution too early, sometimes without considering suitable bankruptcy alternatives.

Keywords:

avoid bankruptcy,debt consolidation,bankruptcy,debt consolidation loan,unsecured debt

Article Body:

In this debt-ridden society, many people are in severe financial difficulties. While bankruptcy is the last step in a long road of financial pressures for many, others opt for this solution too early, sometimes without considering suitable bankruptcy alternatives.

There are several options available for you if you are in debt and do not wish to declare bankruptcy. The most sought-after option is obtaining a debt-consolidation loan and closing all existing credit lines.

Debt consolidation is where you take a new unsecured loan and use the funds to pay off your outstanding debts.

An unsecured debt consolidation loan will help you consolidate all your unsecured debt and avoid bankruptcy. This new money can save you hundreds of dollars per month if you choose to use your loan to pay off existing debt – especially high rate credit cards. Even if you don�t own a home, you could qualify for their debt consolidation loan.

Debt consolidation loans are repayable over a longer term at a relatively low interest rate. This means that the monthly repayments are lower. If the loan is secured on your property then the interest rate and payments may be even lower.

But you must compare the pros and of debt consolidation loans before taking the plunge. There are two options for consolidating debts � either you borrow money to pay off all your debts or seek assistance from a debt consolidation service. The decision on which option will meet your needs has a lot to do with whether you can qualify for qualify for low mortgage rates on debt consolidation loans , and the total amount of debt you need to consolidate.

Borrowing for debt consolidation immediately eliminates multiple debt payments. All debt collection actions eliminated. Most importantly, it won’t impact your credit rating; infact it may help improve your credit rating. Seeking debt consolidation services immediately decreases your monthly payments. It also brings to a stop, and in some cases, eliminates some interest and fees.

By getting this loan and using it to pay off credit cards, you�ll pay much less interest. Once you�ve paid off your credit cards or other debt, you�ll have a fresh start with your finances and can set up a budget within which you can live comfortably without ever having to run up credit card debt again.

Debt consolidation is an excellent tool that can help you manage and decrease your debt when you just can’t seem to do it on your own. There is no way that you can completely fix bad credit without the ability to reduce debt and pay your bills on time. However, once your debt has reached a certain level, this can seem almost impossible to accomplish.

A credit counsellor can provide you with the option of enrolling in a debt management plan, which provides immediate relief and allows repayment of debts without the high fees and negative ramifications of bankruptcy.

However, your choice has to be based upon your financial situation, as well as fit in with your own belief system and lifestyle.

Tinggalkan Balasan